Options Market Data Costs: The Real Price of Running OPRA at Scale

Options market data costs often look lower than equities because exchange fees appear smaller on paper. However, that line item is only part of the story. In practice, much of the cost shows up in the infrastructure and operational load required to keep options data stable under burst conditions—especially for OPRA. The fee line is only the starting point, while the heavier burden comes from ingesting, processing, distributing, and operating OPRA reliably at scale.

In 2026, firms face a heavier burden because OPRA capacity planning explicitly centers on bursts. OPRA measures published projections in messages per 100 milliseconds, and the 10-millisecond interval to reflect utilization during bursts of traffic. OPRA also notes that these projections are for one stream only; firms that take both redundant streams for fault tolerance effectively double the bandwidth requirement.

This blog looks into where those costs accumulate: high-throughput networking, capture, parsing and normalization, fanout, and the day-to-day work of monitoring, replay, and recovery. And why resiliency can multiply the total requirement.

Why Options Market Data Costs Add Up?

Options market data costs can look manageable at first because the most visible line items are exchange and licensing fees. If a firm starts with OPRA, that can make options data appear less expensive on paper than it really is. As the options SIP, OPRA disseminates consolidated quotation and last-sale information from the U.S. options exchanges, which is why many firms use it as the baseline view of the listed options market.

But fee comparisons only tell part of the story. Schedules change, usage matters, and actual spend depends on factors such as display, non-display, redistribution, and connectivity. More importantly, the cost of consuming OPRA at scale is shaped by the infrastructure required to keep up with the feed when traffic spikes.

That distinction matters because OPRA planning is explicitly built around bursts, not just steady-state throughput. OPRA’s published projections are measured in messages per 100 milliseconds, and the 10-millisecond interval is used to reflect utilization during bursts of traffic. OPRA also notes that these projections apply to one stream only, so firms that take both redundant streams for fault tolerance must plan for more bandwidth and more processing headroom.

In short, exchange fees belong in any discussion of options market data costs. But they are only the starting point. Once firms account for high-throughput networking, capture, parsing and normalization, fanout, monitoring, replay, and resiliency, the real price of running OPRA at scale looks very different. That is where costs begin to compound.

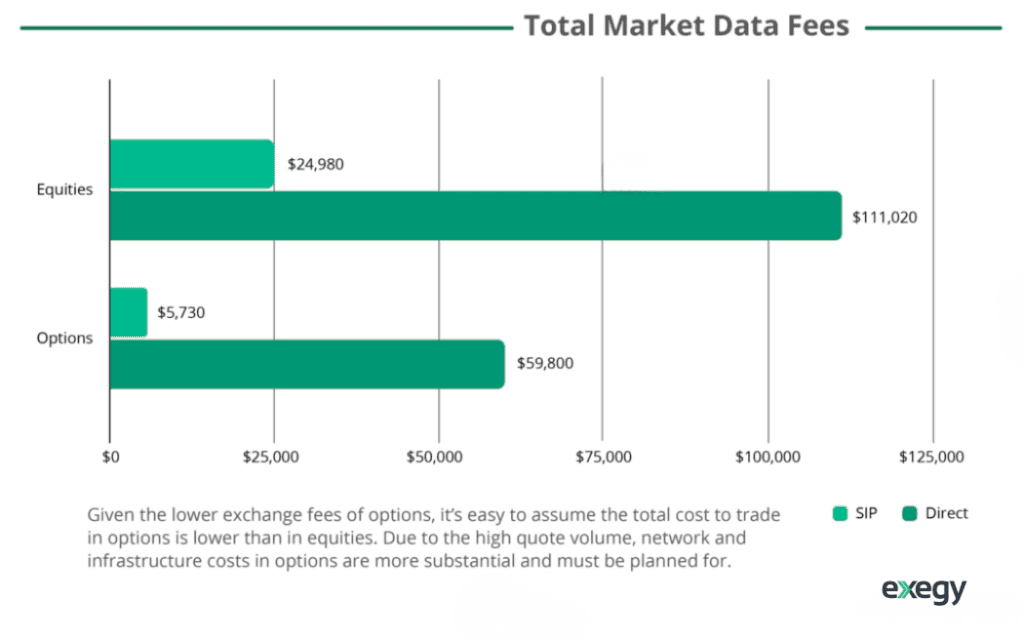

Below is a comparison of SIP and direct feed fees across equities and options. It helps establish the visible cost baseline, but the more important point is that fee schedules do not capture the infrastructure required to process OPRA reliably under burst conditions.

Why Are Options Market Data Costs Often Higher Than Equities?

Despite the low exchange fees, the total cost of options market data is much higher because of the infrastructure burden. In equities, the universe is relatively bounded: one primary symbol per company or fund. In options, every underlying expands into an entire surface of strikes, expirations, calls, and puts. As the underlying moves, liquidity providers update quotes across that surface continuously. With dense strike listings and frequent expirations, even modest price moves can trigger a large number of quote updates across many related contracts.

That is why options feeds, especially OPRA, can behave like a firehose during volatile periods. The challenge is not just the number of instruments, but how quickly activity can cascade across the options chain. Traffic does not arrive as a smooth stream. It arrives in short, intense bursts that place stress on networking, capture, parsing, normalization, and downstream distribution all at once.

OPRA’s own capacity planning reflects that reality. Its published projections are measured in messages per 100 milliseconds, and the 10-millisecond interval is used to reflect utilization during bursts of traffic. In other words, the stress case is not an edge case. It is the design point.

What Are the True Costs of Running OPRA at Scale?

To understand the true costs of options market data, it makes sense to start with the feed most firms use as their baseline: OPRA. As the options SIP, OPRA consolidates and disseminates last-sale information and top-of-book quotations across the U.S. listed options exchanges. For many firms, that makes it the starting point for pricing, monitoring, risk, and surveillance.

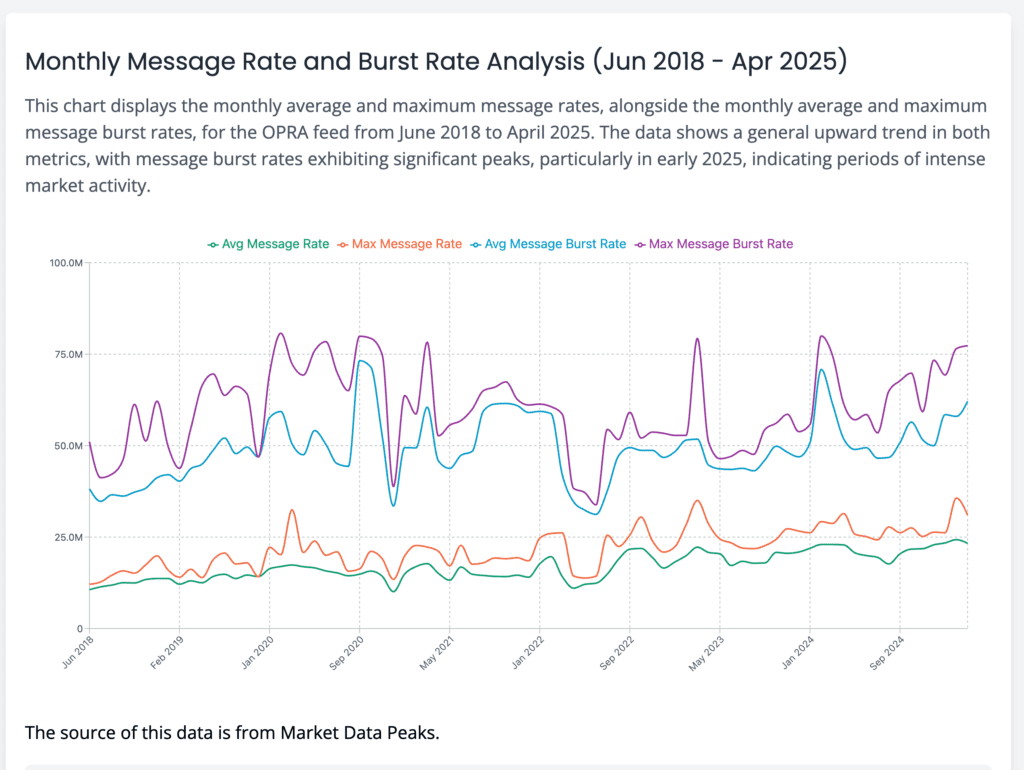

But the real cost of OPRA rarely shows up in the OPRA fee line item alone. It shows up in what it takes to ingest, process, and operate the feed when traffic spikes. Options traffic does not arrive as a smooth stream. It arrives in bursts, and those bursts are where infrastructure starts to strain. Systems sized to daily averages can fall behind quickly when volatility pushes message rates higher across thousands of related contracts.

The chart above helps illustrate the problem. Average OPRA traffic continues to rise, but burst traffic climbs far above that baseline. Infrastructure costs start to compound in that gap because systems are designed for peak conditions rather than average throughput.

This is where the cost picture changes. A firm may be comfortable with average daily throughput, but OPRA does not test systems at the average. The stress comes when volatility compresses activity into short bursts, forcing networks, handlers, and downstream systems to absorb much higher message rates without falling behind.

Matching Consumption Models to Operational Reality

Resiliency adds another layer of cost. Traffic projections apply to one stream only. Firms that take both redundant streams for fault tolerance have to plan for additional bandwidth, additional processing capacity, and more downstream headroom before even accounting for retransmissions, replay, or recovery workflows.

It is also worth separating OPRA fees from connectivity costs. A firm may still incur connectivity and provider costs depending on how it accesses OPRA data, and those costs sit outside the basic OPRA fee line while still contributing to the total cost of running the feed in production.

At that point, the cost discussion starts to look very different. It is no longer just about exchange fees. It is about the full stack required to keep OPRA stable under pressure: high-throughput networking, capture, parsing and normalization, fanout, monitoring, replay, and operational recovery.

For a deeper look at OPRA message-rate trends and burst behavior, download the full report here.

What Do Firms Need from an Options Market Data Solution in 2026?

By 2026, the question is not simply how to get access to OPRA. Most firms can get access. The real question is whether their market data architecture can stay stable when options traffic becomes volatile, bursty, and operationally demanding.

That means firms need more than a feed. They need a way to absorb short bursts in message volume without falling behind, a resilient design that can support redundancy and recovery, and enough operational visibility to monitor the feed when conditions become stressed. In practice, that means thinking about sustained throughput, burst tolerance, replay and gap handling, downstream fanout, and the day-to-day work of keeping a production environment healthy.

For Some Firms, Control Still Matters Most

Some firms choose to build and operate their own infrastructure because they want the highest degree of control over ingestion, normalization, tooling, and performance tuning. That can make sense for firms with highly specialized needs, but it also means owning the long-term engineering and operational burden that comes with OPRA-scale traffic.

Others Prioritize Managed Performance

Other firms use hosted or managed infrastructure to keep much of the performance profile of an in-house environment while shifting hardware, deployment, and day-to-day care to a provider. This can reduce the internal burden on engineering and operations teams while still preserving a high-performance architecture. Exegy positions its Hosted Ticker Plant this way, as a managed option for firms that want low-latency processing without standing up and operating the entire stack themselves.

Some Need the Fastest Path to Consumption

A third model is market data as a service, where firms consume normalized feeds through a managed delivery model rather than building and running the full ingestion environment internally. This approach is often the fastest to deploy and the most operationally efficient because the infrastructure investment and day-to-day maintenance shift to the provider. Exegy’s Axiom is a fully managed market data service that provides normalized data from more than 300 sources while reducing infrastructure investment and operational burden.

How Should Firms Evaluate the Right Fit?

With a clearer view of the true costs of OPRA — not just fees, but also scale, burst handling, resiliency, and ongoing operations — firms can make a more informed decision about which model fits their latency requirements, internal resources, and tolerance for operational complexity.